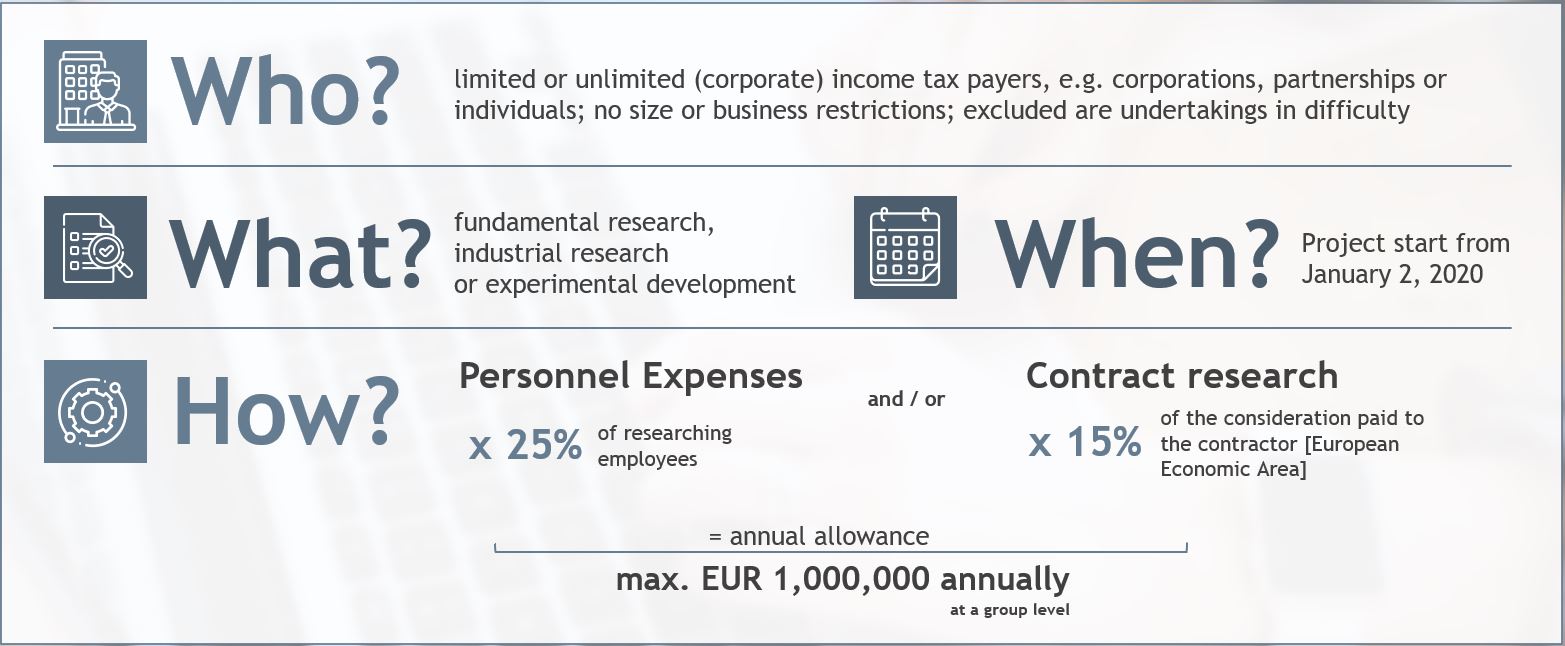

Companies in Germany have been eligible for an annual research allowance of up to EUR 1,000,000 since 2020.

If a company uses its own research staff, 25% of the wages and salaries, including tax-free social security contributions, are credited against the annual tax liability. Any remaining surplus is reimbursed. With the reimbursement, companies can benefit from the subsidy, even in loss-making phases, thereby, e.g., making the research allowance attractive for start-ups with initial losses.

The same applies to contract research. The allowance to which the client and not the contractor is entitled, amounts to 15% of the remuneration paid to the contractor. Although the research allowance also amounts to 25% here, only 60% of the remuneration is taken into account.

We will be happy to support you in checking the prerequisites, the application, the optimal structuring or any further questions. In this regard, we have outlined our consulting offering in the services section. We look forward to receiving your e-mail or your call!

We have compiled further details on the key points for you, below:

Eligible companies

Entities with limited or unlimited tax liability are eligible within the meaning of the Income Tax Act and the Corporation Tax Act, provided they are not tax-exempt and satisfy the other application requirements.

These include sole proprietorships, corporations or domestic permanent establishments. In addition, partnerships are also eligible, even if their income is only subject to income or corporation tax via their partners.

Exclusion of certain companies

The General Block Exemption (GBER) (Commission Regulation (EU) No 651/2014 of 17 June 2014, declaring certain categories of aid compatible with the internal market in application of Articles 107 and 108 of the Treaty on the Functioning of the European Union; OJ L 187 of 26 June 2014 p. 1) excludes certain companies, including companies in financial difficulties, from the tax incentives. Therefore, before submitting an application, it is necessary to carry out an assessment in accordance with the GBER.

Since, according to the explanatory memorandum to the Act, the criteria of the GBER must be fulfilled during the entire funding period, a continuous examination of the relevant key figures and framework conditions is also necessary.

Research and development projects

Research and development projects are eligible for tax concessions provided they fall in one or more of the categories of fundamental research, industrial research or experimental development. The delimitation is made according to the criteria of the General Block Exemption (GBER).

However, projects are not eligible according to these criteria if, for example, a product or process is essentially already established and only market development is the primary objective. The same applies to routine developments - funding is ruled out in this case, too. Applications referring to such projects are regularly rejected.

Consequently, already in the application for eligibility, attention should be paid to the exact project description. This is definitely a challenge in practice, due to the limited text length that can be submitted. Appropriate experience in the formulation is helpful and can significantly increase the chances of a successful application.

Granting

In-house research

Eligible for the tax incentives are the wages of employees who are entrusted with the research, and which are subject to wage tax deduction by the beneficiary, as well as the tax-free expenses (social security contributions) actually incurred to secure the employees' future.

Verifiable documentation must be prepared to provide proof. If employees are not deployed exclusively for a project eligible for funding, this involves administrative effort in view of the division that is then required. In addition to the time sheet provided by the Federal Ministry of Finance, recording via an ERP system or special software solutions is also possible.

Funding is not possible if the company does not conduct research for itself but on behalf of others. However, if the requirements are met; the client could benefit from the research allowance, which could also benefit the contractor if the resulting funding budget at the level of the client is higher.

Sometimes, the border as to whether in-house research is present or not is fluid. Here, for example, contracts in which special products are developed on behalf of a client can lead to in-house research by the researching company or to contract research by the client, depending on how the contract is structured.

Contract research

For contract research, 60% of the remuneration paid to the contractor is taken into account. The percentage represents a flat-rate share that is intended to correspond to the share of labour wages at the contractor. Individual proof of the contractor's personnel expenses is not required and thus cannot lead to a reduction, but also cannot be used to increase the percentage.

Consequently, contract research can be advantageous in the case of capital-intensive research and development activities, since 60% of the remuneration can by far exceed the actually-incurred labour wages. Here, optimisation opportunities arise, because it is irrelevant for the granting of the tax incentives whether the contractor is an external company, a public institution such as a university, or a company from the same corporate group. However, all framework parameters should always be taken into account. Purely by way of example, the subsequent operational use of the know-how gained or transfer prices should be mentioned.

Funding for contract research is not limited to domestic contractors. Eligible projects also include contract research where the contractor has its management in a member state of the European Union or another state to which the Agreement on the European Economic Area (EEA Agreement; where administrative assistance exists) applies.

It must always be ensured that the contracts comply with the necessary requirements. Although the tax authorities do not set their own standards for this, they do refer to the general regulations on contract research. Hence, a prior review of the contracts can prevent a subsequent non-granting of the research incentives and help in securing funding.

Special features for sole entrepreneurs and partnerships

The law provides for special regulations for sole entrepreneurs and partners in a partnership. Here, proven personal contributions by sole entrepreneurs and partners may be eligible for funding at a flat rate (EUR 40 per working hour, maximum 40 working hours per week).

This means that entrepreneurs who are not organised as a corporation and who do not have research employees can also benefit from the tax incentives. In this case, though, the de minimis regulations must be observed, and these may require an examination in individual cases.

Maximum amount and research allowance

The research incentive amounts to 25% of the assessment basis, capped at EUR 4 million, so that a maximum of EUR 1,000,000 can be claimed annually. It should be noted that in 2020 the maximum amount of EUR 500,000 still applies in some cases.

"Affiliated" companies can only receive the maximum amount of funding once, while contractually cooperating companies can each receive it separately. Within this context, affiliated companies are defined by means of the controlling influence pursuant to Section 290 Par. 2 to 4 of the German Commercial Code (HGB).

The research incentive is determined in a separate assessment and is fully credited against the assessed tax in the next first assessment for income or corporation tax of a year. A refund is made if the research incentive exceeds the assessed tax. This way, companies are also directly supported in loss-making stages.

Other expenses may be eligible for support under other funding measures. The law explicitly provides for the possibility of accumulation. However, a double reduction for the same expenses is excluded. For this reason, expenses that have been included in the assessment basis of the research incentive may not have been included in the context of other funding or subsidies, which limits the scope for complementary funding measures for the same project.

Application for funding

The tax incentive is subject to application. After the end of the respective financial year, the entitled person can submit an application for the research incentive to the responsible tax office in accordance with the officially prescribed data set. Entitled partnerships must submit the application to the tax office that takes care of the separate and uniform determination of bases of taxation.

The application to the tax office requires a certificate confirming the eligibility of each research and development project listed in the application. Details are governed by the Research Grants Certification Ordinance (FzulBV) of 30 January 2020.

This certificate must be applied for separately in advance. Owing to the above, it is also referred to as a two-stage application procedure.

For this purpose, the Federal Ministry of Education and Research has created a separate website. The Research Grant Certification Centre (BSFZ) is operated by a consortium of VDI Technologiezentrum GmbH, AIF Projekt GmbH and the German Aerospace Center e. V. - DLR Project Management Agency with locations in Bonn, Berlin, Düsseldorf and Dresden. Information on the application procedure and the official application form are provided on the BSFZ website. The certifying body checks whether the activities described in the application are an eligible project within the meaning of the Research & Development Tax Incentive Act (FZulG).

The certificate issued is generally binding for the tax office.

Entry into force and application

The Act entered into force on 1 January 2020. Beneficiaries are only projects whose work began on or after 2 January 2020 (in-house research) or for which the order was placed after this date (contract research).