News@BDO

Datum:

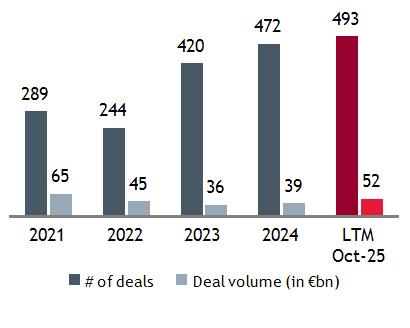

In Q3-2025, a total of 130 transactions in the automotive sector have been observed, which is an increase both from Q2-2025 (111 transactions) and Q3-2024 (114 transactions). Compared to the record high transaction activity in Q4-2024 (139 transactions), deal count slightly decreased by 9 transactions or 6.5 %.

Asian domestic deals made by far the largest contribution to Q3-2025 sector deal flow with 51 transactions. European domestic transactions contributed 19 transactions, followed by North America (17 transactions).

Main drivers of Q3-2025 M&A activity were transactions in the body & chassis, brakes, steering, exterior and interior segments while transactions in the EV segment did contribute to a lesser extent to the quarter’s deal flow activity.

The global automotive sector continues to be affected by US government trade tariffs. In September 2025 the U.S. and EU struck a trade deal, with the U.S. setting the new import tariff for most goods shipped to the U.S. to 15 % (compared to 25 % from April 2025), and zero tariff for most or all U.S. exports to the EU, including autos and auto parts — effective retroactively from 1st August 2025. The 25 % tariffs on steel, aluminum and copper from Section 232 are to remain for now, further affecting automotive suppliers.

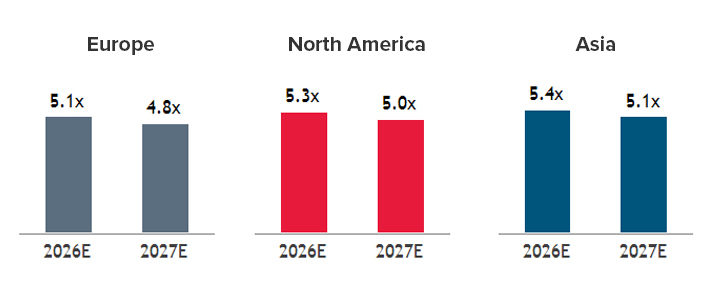

As per November 2025, European automotive suppliers trade at an implied EV/EBITDA 26E multiple of 5.1x (median-based) which is an uplift of 0.7x EV/EBITDA multiple points compared to 4.4x as per BDO’s Q2-2025 valuation analysis.

At the same time North American automotive suppliers’ valuation levels slightly decreased. The implied EV/EBITDA 26E multiple stood at 5.3x (median-based) in November 2025 compared to 5.4x as per the Q2-2025 automotive sector update.

APAC stock-listed automotive suppliers traded at an implied EV/EBITDA 26E multiple of 5.4x compared to 5.0x in the last quarter representing a valuation inflation of 0.4x EV/EBITDA multiple points.

In line with the observed mid-term historic trading pattern, North American stock-listed automotive suppliers continue to deliver share price outperformance over their European and Asian peers. Over the last three years, the North American automotive supplier peer group experienced a total share price appreciation of 60 % compared to 43 % of the APAC peer group and negative 6 % of European peers.

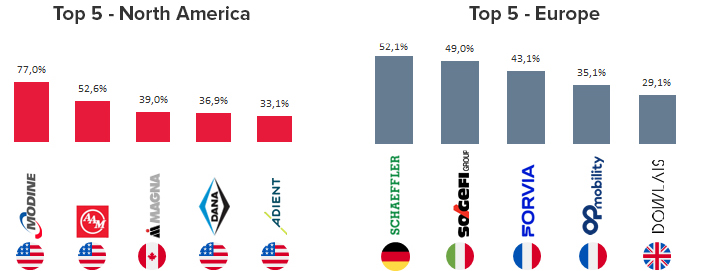

Within our European automotive supplier peer universe, Schaeffler delivered the best share price performance (+52.1 %) over the last six months (as per November 2025). The stock was influenced by broader automotive sector dynamics, including electrification trends and supply chain recoveries (strong order intake in region Greater China and Europe in the area of E-Mobility, as well as in Americas in HEV), as well as operational gains across all company divisions.

In North America, the share price of Modine performed even better (plus 77.0 %) over the same period. The uplift is supported by several factors, including strong performance in company’s Climate Solutions and HVAC segments, robust sales growth and strategic investments and acquisitions to expand its data center cooling capacity.

The electrification trend of the EU vehicle fleet continues in 2025 with 1.5m new BEVs registered per Oct-25 YTD, increasing EU’s total BEV fleet to almost 9m cars now. New registrations of classic petrol or diesel type cars still remain very relevant but steadily decline.

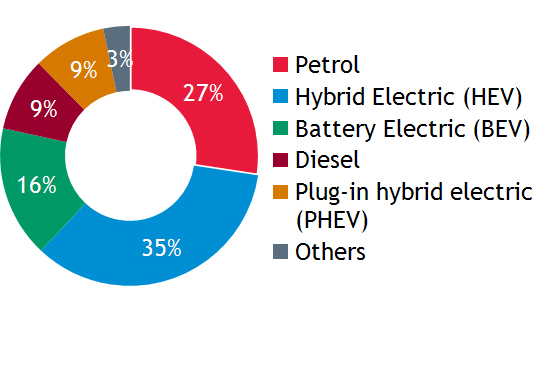

Per Oct-25 YTD, HEVs again lead the charts with a 35 % share of all EU car registrations, followed by petrol (27 %) and BEVs (16 %) while diesel and PHEV both achieve a 9 % share.

BEV registrations in the EU per Oct-25 YTD rose by +301k (+26%) to 1,473k units (vs. 1,172k in Oct-24 YTD).

Among the larger EU markets, the Spanish market achieved high growth rates in terms of both new car registrations (+15 % in Oct-25 YTD) as well as for BEVs in particular (up +90 % vs. Oct-24 YTD).

On the other end, Oct-25 YTD new car registrations in France declined by (-5 %) vs. Oct-24 YTD , although BEV registrations slightly increased.

German car registrations for the same period remained virtually stable (+0.5 %), albeit with a strong increase in BEV registrations (+123k units or +39 % to now 434k per Oct-25 YTD), underlining a shift in consumer sentiment.

Registration to receive the “Automotive Sector M&A Update” and further updates is currently unavailable. We are working on a solution.

In the meantime, please contact our listed team members, who will be happy to provide the “Automotive Sector M&A Update” and further information.

Thank you for your understanding.