Bridging Assistance III will provide support for companies, own-account workers, and freelancers in all sectors with an annual turnover of up to EUR 750 million in the performance period from November 2020 to June 2021. The EUR 750 million turnover ceiling does not apply to companies directly affected by lockdown (retail, events and cultural industries, hotels, hospitality, and pyrotechnics), as well as companies in wholesale and the travel industry.

Application

Applications can only be filed by tax advisors, auditors, and lawyers (auditing third parties) until 31 August 2021.

Eligible Applicants

Companies and non-profit organisations from all sectors of the economy are eligible to apply for Bridging Assistance III. Own-account workers and freelancers who pursue their profession as their main occupation are also eligible to apply. If companies have applied for or already received November or December Assistance, they are not eligible to apply for these two months. In addition, companies belonging to an international group or companies that are not registered at a German tax office are excluded.

Application Requirements

Companies that have suffered a Corona-related slump in sales1 of at least 30 % in one month compared to the reference month in 2019 are eligible to apply and receive funding. The calculation is made separately for each month. If the slump in sales of at least 30 % does not exist, the Bridging Assistance III for the respective month does not apply. The applicant must also not have been in economic difficulties2 on 31 December 2019. Affiliated companies may only submit one application for all of their affiliated companies together.

Qualifying Costs

Bridging Assistance III subsidises certain operational fixed costs incurred during the performance period from November 2020 to June 2021. These include, in particular, rents and leases, interest expenses, depreciation, the interest portion of lease payments, maintenance of fixed assets, real estate taxes, license fees, insurance, and the costs of auditing third parties. In addition, expenses incurred in the eligible period from March 2020 to June 2021 for construction measures up to EUR 20,000 per month for the implementation of hygiene concepts or one-off digital investments up to EUR 20,000 are reimbursed. There are also extensive additional regulations for individual sectors.

Payments within a corporate group or a company split-up are not eligible. Payments from companies to individual shareholders (natural persons) are recognized as fixed costs and are therefore eligible.

Amount of Possible Funding

Bridging Assistance III reimburses a portion of eligible costs equal to

|

90 % of incurred eligible fixed costs in case of slump in sales > 70 % |

|

60 % of incurred eligible fixed costs in case of slump in sales ≥ 50 % and ≤ 70 % |

|

40 % of incurred eligible fixed costs in case of slump in sales ≥ 30 % and < 50 % |

in the eligible month corresponding to the respective month in 2019.

Companies are entitled to receive up to EUR 1.5 million per month. Affiliated companies can apply for a total of up to EUR 3 million in assistance per month.

Eligible applicants who submit the application via an auditing third party receive a down payment of 50 percent of the requested funding (maximum EUR 100,000 per month or up to EUR 800,000 in total).

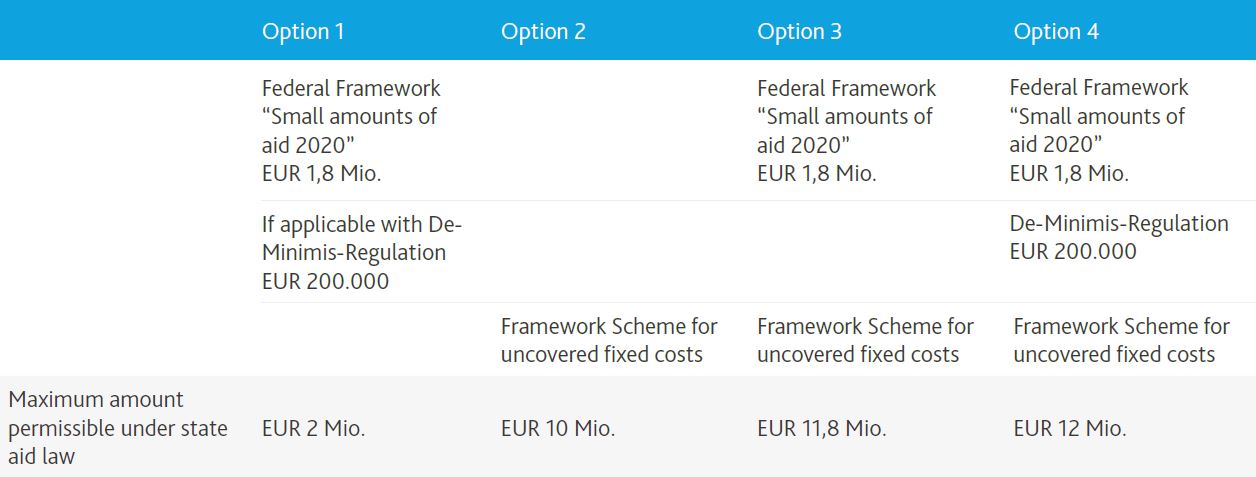

Limitations under State Aid Law

The maximum aid limits of currently EUR 12 million may not be exceeded with all coronavirus-related assistance programmes used, e.g. KfW fast loan, emergency assistance, November/December Assistance, and bridging assistance.

Bridging Assistance III may be based on either the Federal Framework “Small amounts of aid 2020” (“Bundesregelung Kleinbeihilfen 2020”) (cumulatively with the De-Minimis Regulation, if applicable), the Framework Scheme for aid in the form of support for uncovered fixed costs (“Bundesregelung Fixkostenhilfe 2020”), the two federal regulations cumulatively, or all three bases. Thus, there are the following options available to choose from:

The other preconditions of the individual aid regulations must be observed. For example, the Framework Scheme for aid in the form of support for uncovered fixed costs requires uncovered fixed costs. Essentially, these are all fixed costs that are not covered by the contribution margin from revenues or from other sources (e.g., other aid) in the eligible period and thus lead to a loss situation. In addition, the total amount of aid may not exceed a certain size of uncovered fixed costs, 90 % for small or micro enterprises and 70 % for all others.

Miscellaneous

The application for Bridging Assistance III is generally made on the basis of forecasts. The loss in sales, fixed costs and uncovered fixed costs within the meaning of state aid law that have been incurred and are eligible for consideration are then reported at a later date as part of the final settlement. This may result in further payments or even reimbursements.

Even though the assistance does not have to be repaid in principle, the Bridging Assistance III is taxable and must be taken into account in accordance with the general tax regulations as part of the profit determination. In the event of an overlap of other assistance programmes with the same funding purpose and period, any assistance already paid will be offset.

If the company is not going to continue operating until June 2021, the financial assistance must be reimbursed. For companies that have ceased operations or filed for insolvency, payment of the assistance is excluded.

Further Information (in English and other languages)

|

|

Economic impact of the coronavirus:

|

Further Information (only in German)

|

|

|

1 Sales are taxable sales pursuant to § 1 UStG.

2 Regulation (EU) No. 651/2014 (General Block Exemption Regulation).