News@BDO

Date:

The global automotive supplier sector continues to operate in a structurally impaired environment.

A flattish global light vehicle production volume outlook for 2026 as well as geopolitical tensions such as the US/Iran conflict and US tariffs severely drag on demand. While the recent sky rocketing oil prices are supportive to the general transformation towards vehicle electrification, at the same time the (European) BEV sector severely suffers from a surge of Chinese BEV exports into mainland Europe in an attempt of Chinese BEV OEMs to escape from intensifying domestic competition.

As a result, automotive suppliers will remain under pressure from increasing OEM “cost pass through”, shortage of qualified labour, and (most likely) increasing interest rates over time. As such, an increasing gap between winners and laggards becomes visible as a result of a structural shift in automotive value pools and the ever rising importance of electrification, electronics, and software.

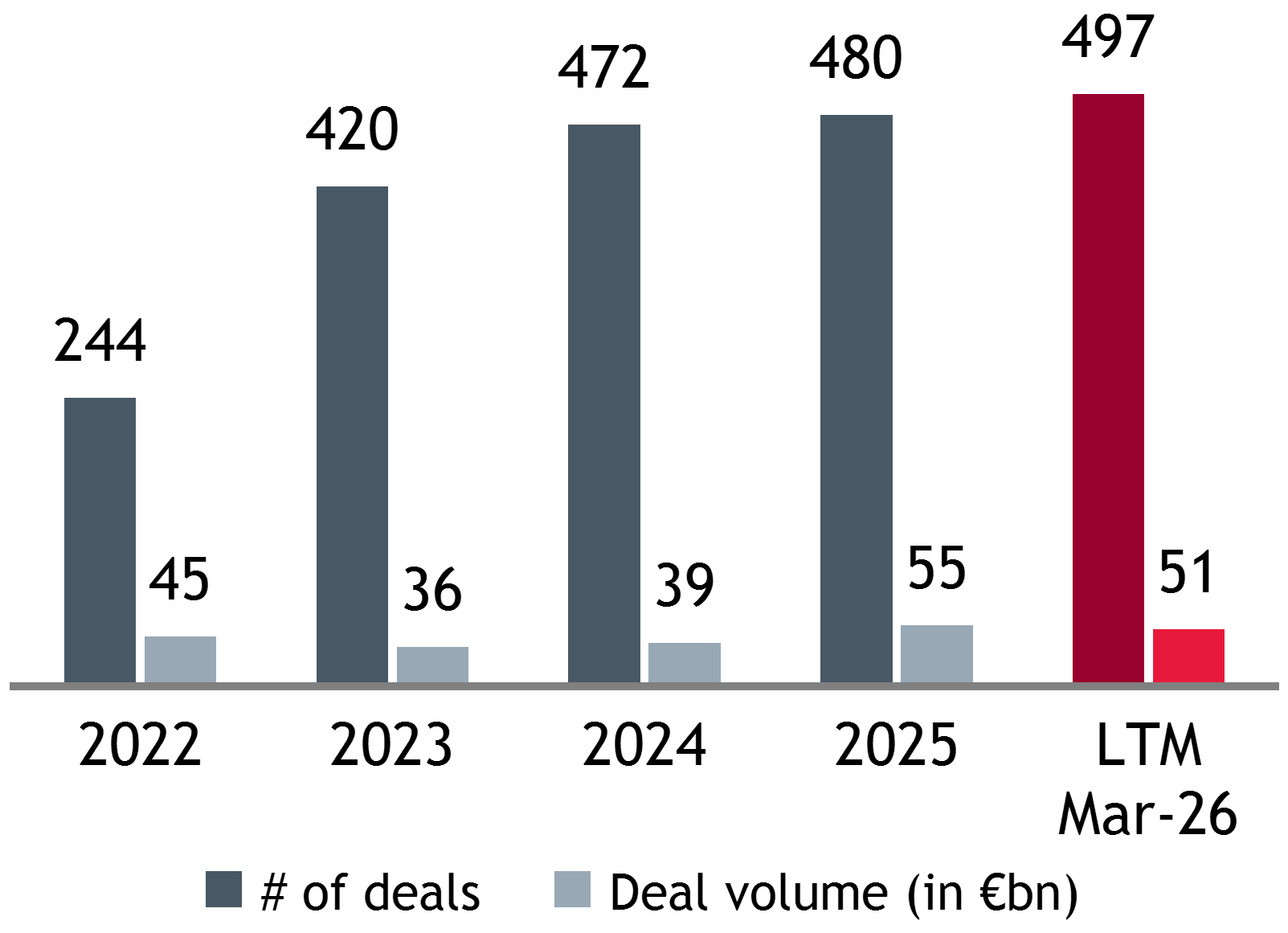

In Q1-2026, we observed a total of 130 transactions in the global automotive sector, which is in line with the previous quarters’ deal activity (126 in Q4-25, 130 in Q3-25).

Asian domestic deals made the largest contribution to Q1-2026 sector deal flow with a total of 53 transactions. European domestic transactions contributed 41 transactions, followed by North America with 18 transactions.

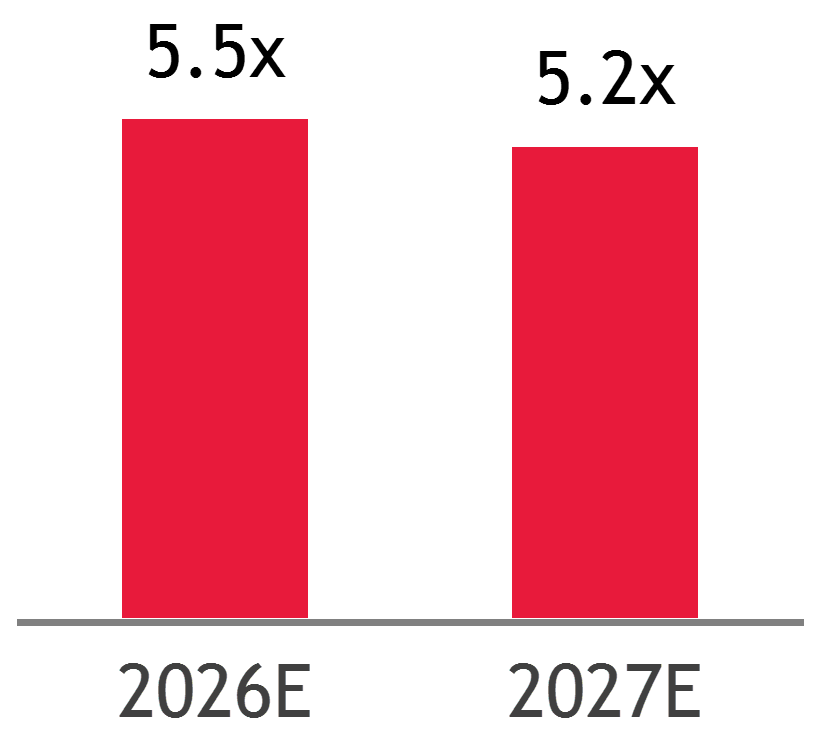

As per April 2026, European automotive suppliers trade at an implied EV/EBITDA 26E multiple of 5.4x (median-based) which is an increase of 0.6x EV/EBITDA multiple points compared to 4.8x as per BDO’s Q4-2025 valuation analysis.

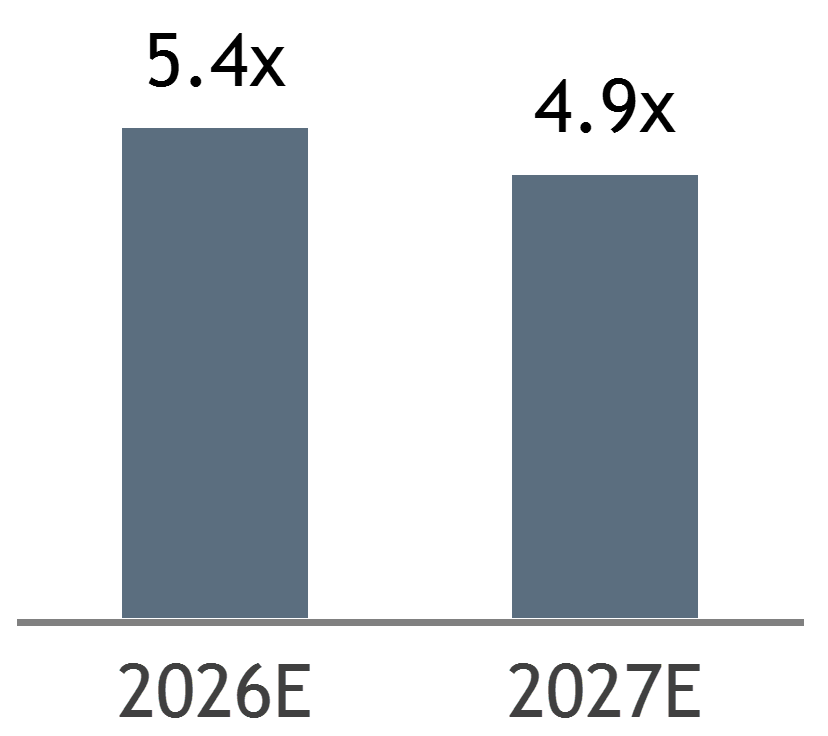

At the same time North American automotive suppliers’ valuation levels decreased. The implied EV/EBITDA 26E multiple is at 5.5x (median-based) in April 2026 compared to 5.9x as per our Q4-2025 automotive sector update.

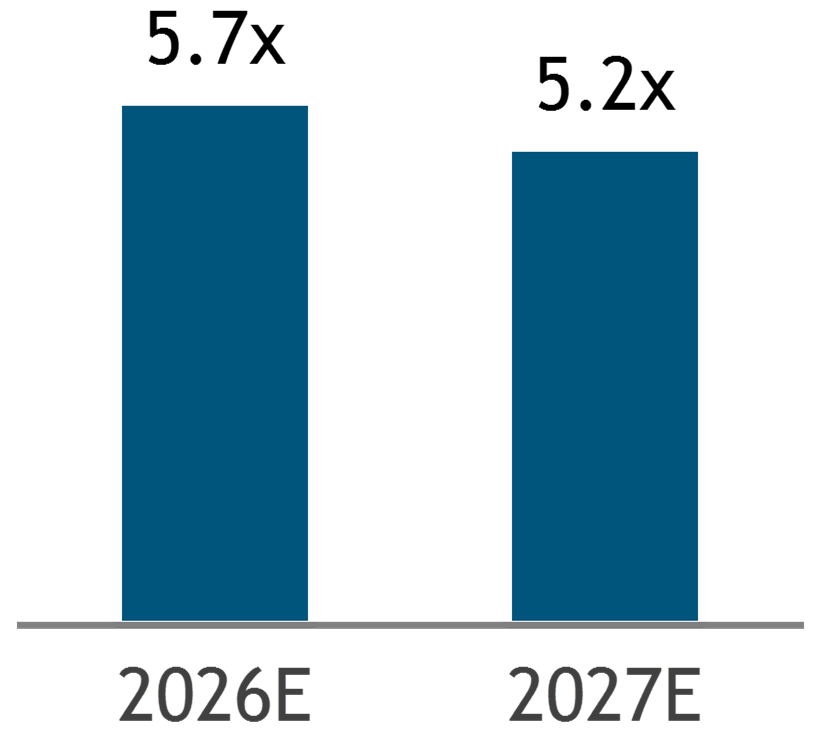

APAC stock-listed automotive suppliers trade at an implied EV/EBITDA 26E multiple of 5.7x compared to 5.9x in the last quarter representing a small valuation decrease of 0.2x EV/EBITDA multiple points.

Europe

North America

Asia

In line with the observed mid-term historic trading pattern, North American stock-listed automotive suppliers continue to deliver share price outperformance over their European and Asian peers. Over the last three years, the North American automotive supplier peer group experienced a total share price appreciation of 127% compared to 53% of the APAC peer group and a negative 13% of European peers.

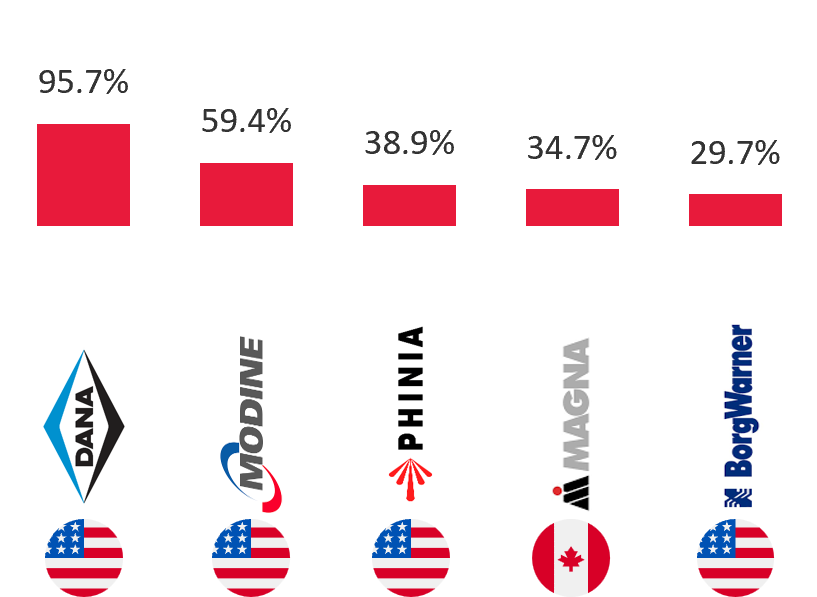

Top 5 — North America

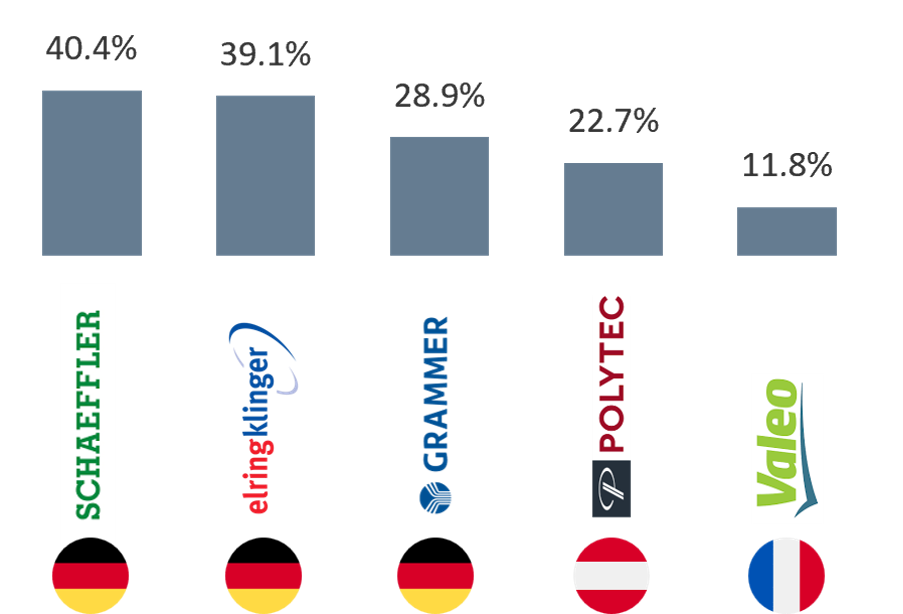

Top 5 — Europe

Within our North American automotive supplier peer universe Dana is the best performing share, rising by plus 95.7% over the last six months (as per April 2026). Dana recently announced a new long-term strategy Dana 2030, designed to accelerate profitable growth. The Dana 2030 strategy envisages approx. $10bn in sales by 2030 (+33% compared to FY26 sales guidance), a higher adj. EBITDA margin of 14-15% (+400 basis points above 2026 guidance), higher FCF targets as well as a $2bn share repurchase program through 2030 beyond the $765m already completed.

At the core, the Dana 2030 strategy focuses on a total of five pillars: Three pillars are focused on profitable growth, namely Traditional Products Growth (leveraging Dana’s core capabilities in installed ICE capacity, new program wins, and benefitting from overall market recovery tailwinds), Aftermarket Growth (increase market share in e.g. sealing products) and Applied Technologies Growth (targeting high value markets such as EV and defense, leveraging existing portfolio and capabilities into in new markets and products). Further two pillars focus on margin enhancement, namely Manufacturing Excellence (through automation, manufacturing optimization) and Structural Cost Reduction (optimizing processes, organizational alignment)

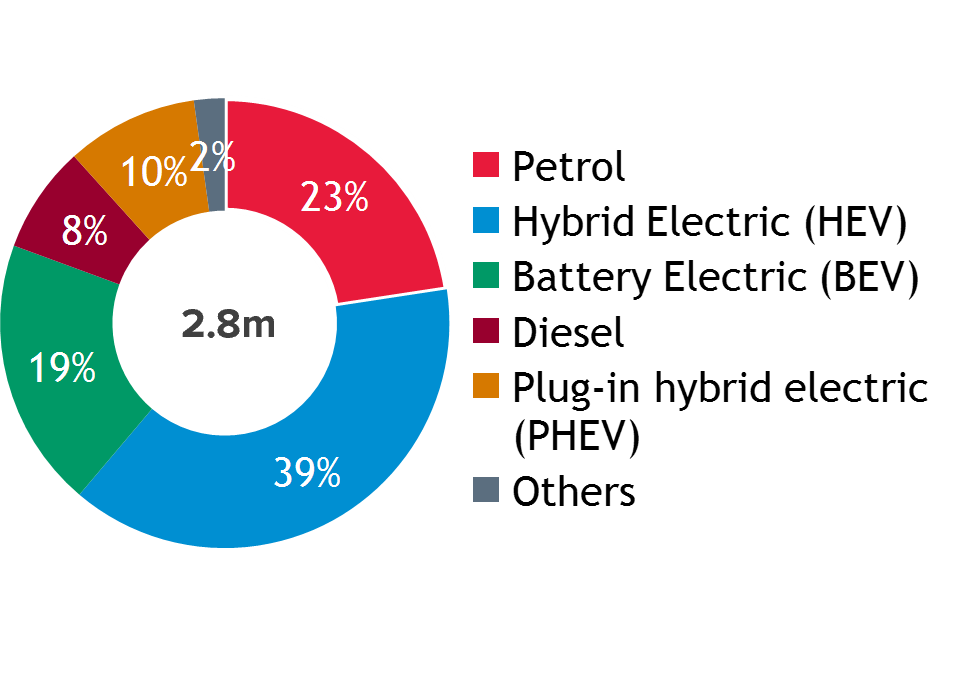

The electrification trend of the EU’s vehicle fleet continued with a total of 547k newly registered BEVs in Q1-2026. Total BEV registrations in the EU in Q1-2026 rose by +134k (+33%) to 547k units (vs. 413k in Q1-2025).

In Q1-2026, HEVs led the charts with a 39% share of all EU car registrations, followed by petrol (23%), BEVs (19%), diesel (8%) and PHEV (9%).

New car registrations of classic petrol or diesel type cars remain very relevant but continue to steadily decline. Monthly petrol type registrations are down -9.4% y-o-y to ~262k, diesel type registrations down -12.3% y-o-y to ~83k).

Among the larger EU markets, German car registrations increased moderately by +5.2% compared to Q1-2025, but show a significant increase in BEV registrations (+47k units or +41% to now 160k per Q1-2026), underlining a shift in consumer sentiment.

Registration for future Automotive Sector M&A Updates will be made available again shortly.