Publication

Date:

On 29 October 2025, the European Banking Authority (EBA) published its final Regulatory Technical Standards (RTS) specifying how institutions must assess the materiality of Credit Valuation Adjustment (CVA) risk stemming from securities financing transactions (SFTs) measured at fair value: EBA/RTS/2025/07.

The RTS introduces a harmonized, quantitative test that determines when SFT-related CVA risks must be included in capital requirements under Article 382 CRR.

Under CRR3, institutions are required to include CVA risk from SFTs in capital requirements when these risks are considered material. Until now, materiality assessments relied heavily on supervisory judgement, which often resulted in SFTs being excluded from CVA calculations due to the absence of a clear standard.

The new RTS (issued under Article 382(6) CRR) sets out binding criteria, conditions, and the frequency for carrying out materiality assessments. Only SFTs measured at fair value under the relevant accounting framework of the institution fall within scope. SFTs that qualify for existing CVA exemptions (Article 382(3) and (4) CRR) generally remain out of scope unless institutions apply them voluntarily.

The RTS introduces a quantitative approach to determine whether SFT-related CVA risk is material:

These changes increase comparability across institutions and eliminate prior ambiguity in supervisory expectations.

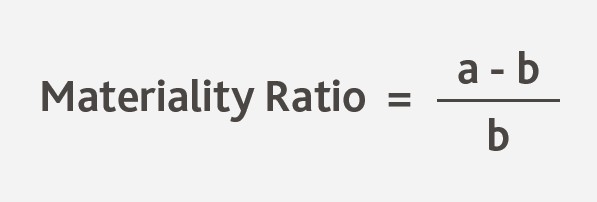

The RTS mandates a simple and transparent ratio comparing CVA capital requirements with and without fair-value SFTs:

where:

a: total own funds requirements for CVA risk including fair-valued securities financing transactions,

b: total own funds requirements for CVA risk excluding fair-valued securities financing transactions.

We offer efficient and flexible calculation capabilities for both BA-CVA and SA-CVA, enabling capital requirement assessments, scenario analyses, and dry-run calculations for the new RTS without requiring changes to your existing systems. This allows institutions to determine potential impacts, assess materiality, and understand capital effects quickly and reliably.

In addition to the calculations, we support you across the full implementation of the RTS requirements. This includes the materiality assessment itself, the analysis of fair-value SFT populations, and the integration of the results into your reporting, control and governance processes. With experience from numerous CVA and CCR projects, we help you implement the new rules in a pragmatic and reliable way.