If a property is used for both turnover entitling to input tax deduction and turnover excluding input tax deduction, the expenses associated with the property must either be apportioned to the respective turnover or divided appropriately according to the percentage of use of the entire building. This topic is extremely relevant in practice in VAT law. In its circular of October 20, 2022, the German Federal Ministry of Finance therefore takes a fundamental position on the apportionment of input tax for mixed-use properties and thus also implements the case law of the German Federal Fiscal Court and the European Court of Justice in this regard.

Direct Assignment Option

As far as possible, expenses incurred for the use, maintenance and upkeep of mixed-use buildings must first be directly apportioned to the turnover that entitles or excludes the deduction of input tax. In this respect, the input tax deduction is either possible in full or not at all.

In the case of acquisition or production costs of a mixed-use building, the German Federal Ministry of Finance excludes a direct apportionment.

Appropriate Apportionment Key

If a direct apportionment of the expenses is not possible, the input tax amounts are to be apportioned appropriately. Likewise, the input tax amounts incurred on acquisition or production costs are to be divided appropriately into a deductible and a non-deductible part according to the percentage of use of the entire building. This applies even if the acquisition or production costs are directly attributable to a commercial unit of a building that is otherwise used for mixed purposes.

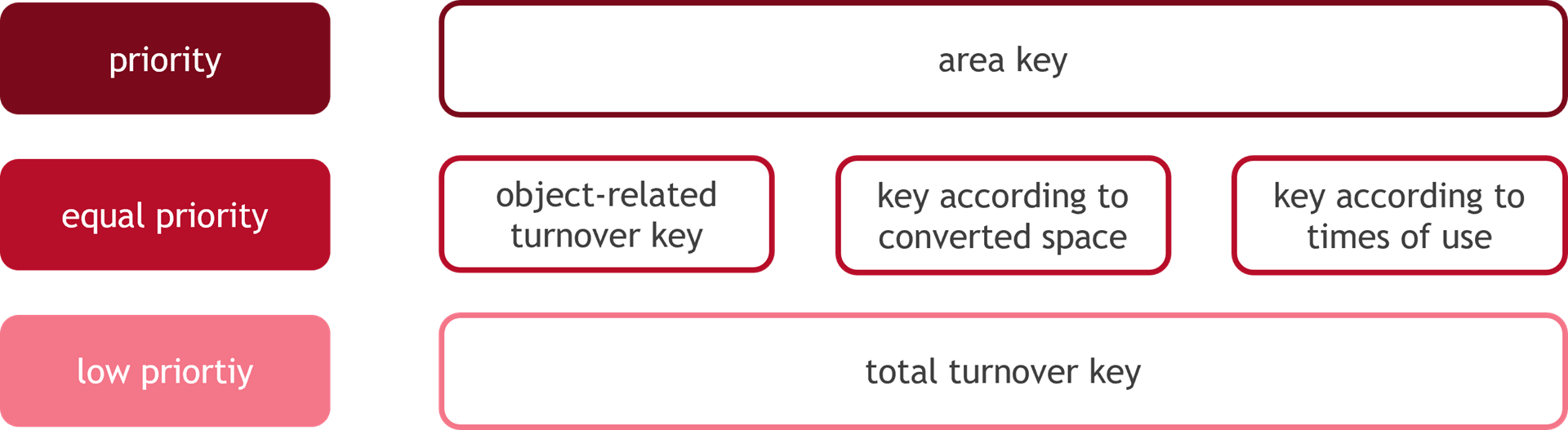

According to the circular of the German Federal Ministry of Finance, various apportionment keys can be considered for an appropriate apportionment, which are, however, in a certain order of priority and partly also subject to certain prerequisites:

The area key (= input tax apportionment according to the relation of the usable areas of the building) is to be applied primarily. This is because, in the opinion of both the German Federal Fiscal Court and the German Federal Ministry of Finance, this is generally the most economically precise method of apportionment.

The area key is determined according to the internal areas of the building, so that external areas are generally not to be included. However, an exception applies to terraces and balconies, which are included at 50 % in the calculation. Regardless of whether residential or commercial space is involved, the floor areas of all rooms are to be taken into account; rooms with sloping roofs are fully considered. Areas used to supply the building or only used in common (e.g. technical rooms, staircase, bicycle storage rooms, laundry rooms) are not taken into account, nor are rooms that have not been developed.

It is possible to deviate from these calculation principles and to use other recognised methods for calculating floor space, such as according to the Living Space Ordinance or DIN 277. However, the prerequisite for this is that this is done uniformly for the entire building, that this method is also used for other (e.g. rental contract) purposes and that the result is appropriate.

Only if the area key does not guarantee an appropriate apportionment the other apportionment keys, with the exception of the total turnover key, can in principle be used on an equal priority basis. However, the tax authorities are entitled to check the selected apportionment key for appropriateness and, in this context, to demand cooperation from the taxpayer.

The object-related turnover key can be considered in the case of significant differences in the equipment of the differently used rooms. Such differences exist in particular in the case of significantly different construction costs, e.g. if the thickness of the ceilings and walls or the interior equipment differ considerably or if some rooms are luxurious while others are only simply equipped. If, on the other hand, differences in equipment are only necessary due to the different use or if they serve a comparable function but do not lead to different expenses, the differences are not significant, with the consequence that the object-related turnover key is excluded.

The apportionment key according to converted space can be considered above all in the case of different storey heights. If the same areas are used alternately at different times (e.g. in the case of a school sports hall), an apportionment key according to times of use is most appropriate.

An apportionment according to a total turnover key is always subordinate and can only be made if no other, more precise key is available.

Notice:

From the point of view of the German Federal Ministry of Finance, the area key continues to be the primary apportionment key for mixed-use buildings. In practice, however, there will often be considerable differences in the equipment. For example, rented residential rooms are regularly less well equipped technically than office or commercial rooms. Consequently, the object-related turnover key is the more precise apportionment key. This is usually more favourable for the taxpayer, as office or commercial rents are usually higher than residential rents.

However, evidence must be submitted that proves the significant differences in the equipment. In the opinion of the German Federal Ministry of Finance, this should be based in particular on a significant difference in construction costs. However, the broad interpretation of the terms “luxurious” or “simple” may lead to disputes between the taxpayer and the tax authorities, which may only be clarified by way of a tax court proceeding.