Updates

Date:

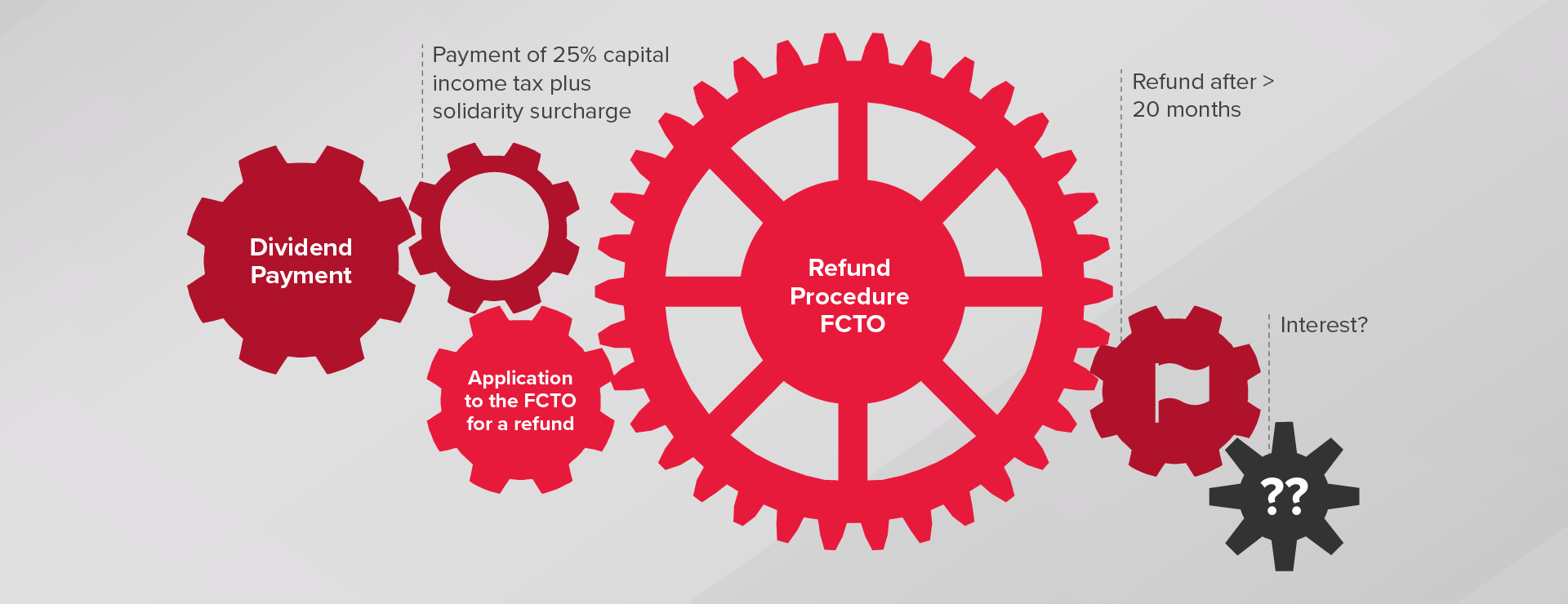

Excessively long refund procedures at the Federal Central Tax Office (FCTO) lead to significant liquidity disadvantages for those entitled to a refund. According to the recently published audit findings of the Federal Audit Office dated 28 April 2026, the FCTO had already warned years ago of potential interest claims under EU law of refund creditors. The Federal Audit Office has now quantified the fiscal risks associated with these persistently long refund procedures at the FCTO concerning withholding tax on dividends (see already BDO Insight) and – in the absence of national regulations on interest on refunds of withholding tax on dividends – has identified a clear area requiring legislative action.

In the absence of a certificate of exemption, tax must be withheld in Germany on dividends paid to foreign shareholders even if Germany has no right of taxation under EU law respectively the Parent-Subsidiary Directive. According to case law, this two-step procedure of withholding and subsequent refund is, in principle, compatible with EU law. Consequently, in this scenario, the foreign company is limited to pursue the refund procedure via the FCTO (see most recently BDO Insight), even in EU cases:

As early as 2024, the processing of a refund application for overpaid withholding tax on dividends at the FCTO took over 20 months. The Federal Audit Office has now confirmed the experience from daily practice that this processing time has not been reduced since then. In fact, the measures taken (see the already published BDO Insight) are said to have merely slowed the growth of the backlog.

By law, refund claims relating to withholding tax are generally not subject to interest (see Section 233a para. 1 sentence 2 of the German Fiscal Code (AO)). An exception applies to refunds of withholding tax that are to be refunded under Section 50g of the German Income Tax Act (ITA) (implementation of the so-called Interest and Royalties Directive). However, there is no corresponding national provision regarding refunds of withheld and paid withholding tax on dividend under EU law. The significant liquidity disadvantages are thus not adequately compensated. It is therefore not surprising that interest claims against the FCTO are now also being asserted in court and that corresponding test cases are pending.

In its decision of 13 March 2024 (case no. I R 1/20), the Federal Fiscal Court had already commented on the reasonable processing time for a refund procedure and affirmed the right to interest on refunds of withholding tax which was levied on dividends against EU law (see BDO Insight). However, this decision concerned the application of the German Investment Tax Act 2004 (InvStG) and a therewith related breach of the free movement of capital.

Furthermore, according to the Federal Fiscal Court decision of 25 February 2025 (case no. VIII R 32/21), interest must be paid on refund claims under EU law if the shareholder was initially denied a refund of withholding tax on dividends by the FCTO with reference to Section 50d para. 3 ITA 2007 (see BDO Insight).

Regarding interest claims due to an excessive length of proceedings in relation to the refund of withholding tax on dividends or withholding tax in general, no judgment has yet been issued by the Federal Fiscal Court.

Against this background, the statements in the audit findings of the Federal Audit Office are particularly noteworthy. Not only does the Federal Audit Office refer to the case law of the Federal Fiscal Court and the pending test cases, but it also goes even further and states that a duration of more than 20 months of a refund procedure raises serious doubts as to whether an effective refund procedure under EU law still exists. Furthermore, the resulting loss of liquidity is considered unacceptable.

It therefore sounds like a wake-up call that the Federal Audit Office is drawing attention to the risks of interest claims under EU law due to excessively long proceedings and is urging the German Federal Ministry of Finance to introduce legal provisions, in particular regarding the question of the applicable interest rate, which has not yet been decided by the highest court.

According to the audit findings, the refund volume for the applications known to the FCTO (i.e. 92,000 out of 122,000 pending applications) amounted to €5.2 billion. The interest loss resulting from this alone was estimated at up to €312 million per year.

Given the number of pending applications and the long processing times at the FCTO, it is all the more important to ensure that all necessary documents and information are properly prepared and enclosed when submitting an application, in order to provide adequate evidence of the entitlement to relief and to avoid any delays caused by queries from the FCTO.

In addition, it must be checked whether, on the basis of EU law, a potential interest claim exists and should be claimed accordingly. This also applies to refunds already received, provided that any potential interest claim has not yet become time barred.

In this context, it is also worth noting the recent decision of the Federal Fiscal Court of 3 March 2026 (case No. VIII R 8/24), in which the FCTO was likewise unsuccessful in a refund procedure under the Parent-Subsidiary Directive. The Federal Fiscal Court confirmed that distributions of profits arising in periods prior to the commencement of liquidation but distributed after its commencement also fall within the scope of the Parent-Subsidiary Directive (see BDO Insight). In this respect, interest claims under EU law are also conceivable in this context.

The dualism of relief from German withholding tax, comprising the refund and exemption procedures, enables eligible claimants to act at an early stage and avoid becoming tied up in lengthy refund procedures. Your contact partners at BDO will help you identify where action is required and support you with the procedures at the FCTO.