Decision of the BFH

Reductions in profits arising from interest receivables relating to legal transactions of an equity-like nature are not covered by either sentence 4 or sentence 7 (now sentence 8) of Section 8b (3) KStG. This is because interest receivables are not tax-exempt as current expenses under Section 8b (2) KStG and do not, in economic terms, take the place of a share. Nor are the interest claims arising in the present case as remuneration for the provision of capital economically comparable to the granting of a loan; there is no loan-like legal relationship concluded for a specific term. However, the inclusion of interest claims (in other circumstances) may be justified if they are converted into a loan by novation or deferred for an unusual period, and the creditor subsequently defaults on them.

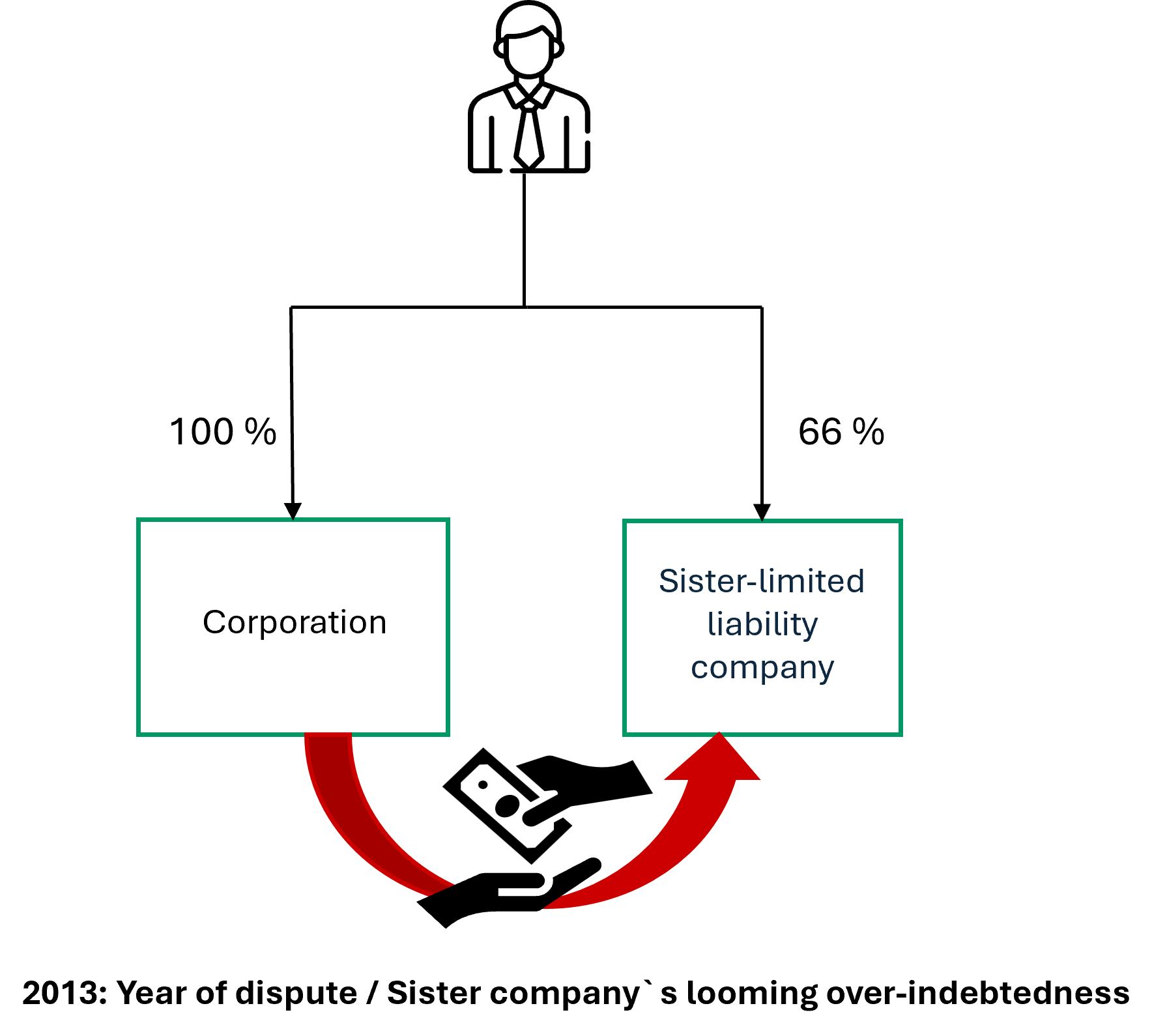

Contrary to the view of the Fiscal Court, the prohibition on deduction under section 8b (3), sentence 4 and 5 KStG does not apply to loan claims where the relationship between the lender and the borrower is mediated by a significant shareholding held by a natural person. This follows from the wording of sentence 5, which, with reference to the fourth sentence, extends the provisions set out therein to persons ‘close to that shareholder’ within the meaning of Section 1 (2) AStG. In this respect, only the shareholder within the meaning of the fourth sentence can be meant, and therefore not a natural person.

This is also supported by the regulatory symmetry achieved in this respect between profits and losses, in that Section 8b (3) sentence 3 KStG refers to reductions in profits in connection with the shares mentioned in paragraph 2. The basic prerequisite is that a corporation is the shareholder realising capital gains or losses. The prohibition on deduction under section 8b (3) sentence 4 KStG builds systematically on sentence 3. Without altering the identity of the shareholder, it does not apply in cases giving rise to substance-related reductions in profits where a natural person is a shareholder of both parties to the loan. This is not precluded by the purpose of the fifth sentence, which is to prevent abusive circumvention arrangements by extending the personal scope of application of the prohibition on deduction regarding the identity of the lender.

The BFH nevertheless referred the case back to the Fiscal Court, as the latter had not made sufficient findings to assess whether a hidden distribution of profits had taken place. Such a distribution may exist from a company granting a loan or providing security to a shareholder if the relevant loans and/or security arrangements between affiliated companies do not satisfy the arm’s length principle. In the examination of the case now to be carried out by the Fiscal Court, it must, in accordance with the principles governing the burden of proof, take into account that it was not the corporation that had to prove that the granting of the loan was in line with arm’s length principles, but rather the tax office that had to prove that it was not.

Notice

The BFH decision sends a positive signal regarding loans granted between sister companies where a natural person is a significant shareholder. The BFH clearly rejects a broad interpretation of the deduction prohibition under Section 8b KStG in such scenarios. However, this does not preclude a profit adjustment due to hidden distributions to the common shareholder – a situation frequently overlooked in triangular arrangements but which does occur. In practice, such intra-group financing arrangements should be structured in such a way that an arm’s-length third party would have granted the loans or allowed the loan claim to stand under otherwise identical circumstances.