Updates

Date:

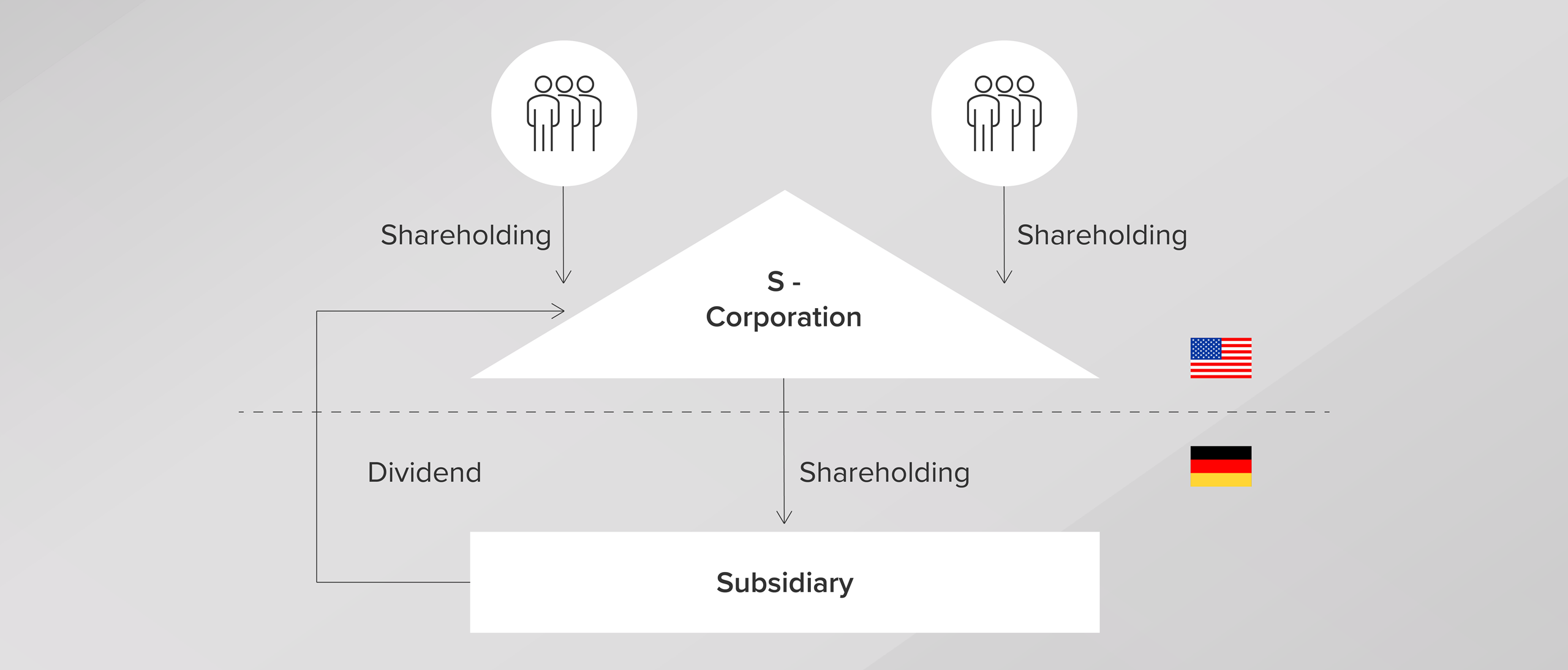

U.S. small and medium-sized businesses are often structured as so-called S-Corporations: Individuals who are tax residents of the United States hold an interest in a U.S. corporation, which in turn owns subsidiaries, particularly abroad - for example, a GmbH based in Germany. The U.S. corporation files an application under Subchapter S of the U.S. tax code (hence the name “S-Corporation”) to qualify for transparent taxation in the U.S. This means that the U.S. corporation’s income is not taxed at the corporate level but rather at the level of its shareholders (individuals).

From a German tax perspective, however, the S-Corporation is regarded as a corporation and thus as non-transparent. It therefore constitutes a hybrid entity.

For a long time, there was disagreement over the rate of withholding tax applicable to dividends paid by a subsidiary based in Germany to an S-Corporation. Basically, the double taxation treaty between Germany and the United States provides for a tax rate of 15% when dividends are distributed to individuals resident in the United States. If the dividend is distributed to a U.S. corporation, generally a tax rate of 5% applies, or in some circumstances even 0%.

In its decision of June 26, 2013 (Case No. I R 48/12, BStBl II 2014, 367), the BFH had already ruled that in these cases, the withholding tax rate for corporations (5% or 0%) generally applies, because the sole determining factor is the classification of the S-Corporation as a corporation from a German perspective.

For distributions made after June 30, 2013, Section 50d (1), sentence 11 of the German Income Tax Act (EStG) (since incorporated verbatim into Section 50d (11a) EStG) was therefore introduced. This provision stipulates for hybrid entities that “the right to … a refund … is available only to the person to whom the investment income … is attributed as income or profits of a resident under the tax laws of the other contracting state.”

Consequently, the question arose as to the effect the former version of Section 50d (1), sentence 11 EStG, introduced in 2013, has:

In its decision of November 16, 2022 (Case No. 2 K 750/19), the Cologne Fiscal Court held that Section 50d (1), sentence 11 EStG, as previously in force, had only procedural effect. The BFH confirmed this in its decision of March 11, 2026 (published on May 28, 2026; Case No. I R 13/23).

With regard to treaty law, the BFH upholds the 2013 decision: Although an S-Corporation is a hybrid entity, it is eligible for treaty benefits.

The national provision of Section 50d (1), sentence 11 EStG (old version) does not alter this, as, in the BFH’s view, it has no substantive legal effect and does not result in a shift of attribution under domestic or treaty law. The legal consequence of the provision is thus limited to determining which person was actually able to assert the treaty-based claim.

In the case of S-Corporations, the tax rate for corporations (5% or 0%) therefore applies; however, the entitlement must be asserted by the individual behind the corporation.

The BFH’s affirmation of the (lower) fiscal court’s decision has resolved the legal uncertainty that previously existed and has set limits on the tax authorities’ pro-fiscal stance. The decision has yet to be published in the Federal Tax Gazette, which is required for it to be applied by the tax authorities. Until then, it is important to keep such cases open and to claim the tax rate applicable to corporations (5% or 0%).