Updates

Date:

A – non-standardised by law – hidden contribution is a company law-related contribution of a contributable and therefore accountable financial advantage by a shareholder (or a person closely associated with them) without appropriate consideration, which a non-shareholder would not have granted to the company when applying the diligence of a prudent and conscientious businessperson. A hidden contribution is generally income-neutral for both the contributor and the recipient company. However, if it has reduced the contributor's income, the recipient company's income increases accordingly (Section 8 (3) sentences 3 and 4 of the German Corporation Tax Act (KStG)). The hidden contribution of shares in one corporation to another is equivalent to their sale. The hidden contribution of a shareholding held as private assets is thus treated as equivalent to that held as business assets, thereby preventing shareholders from contributing a shareholding held as private assets to another company and later selling the shares in that company without incurring a taxable capital gain equal to the increase in value resulting from the hidden contribution. In its practical decision of November 19, 2025 (case no. I R 40/23), the German Federal Fiscal Court (BFH) clarified whether a hidden contribution of shares in a corporation reduces the shareholder's income even if taxation was incorrectly omitted under substantive law and the income tax assessment issued to the contributor can no longer be changed.

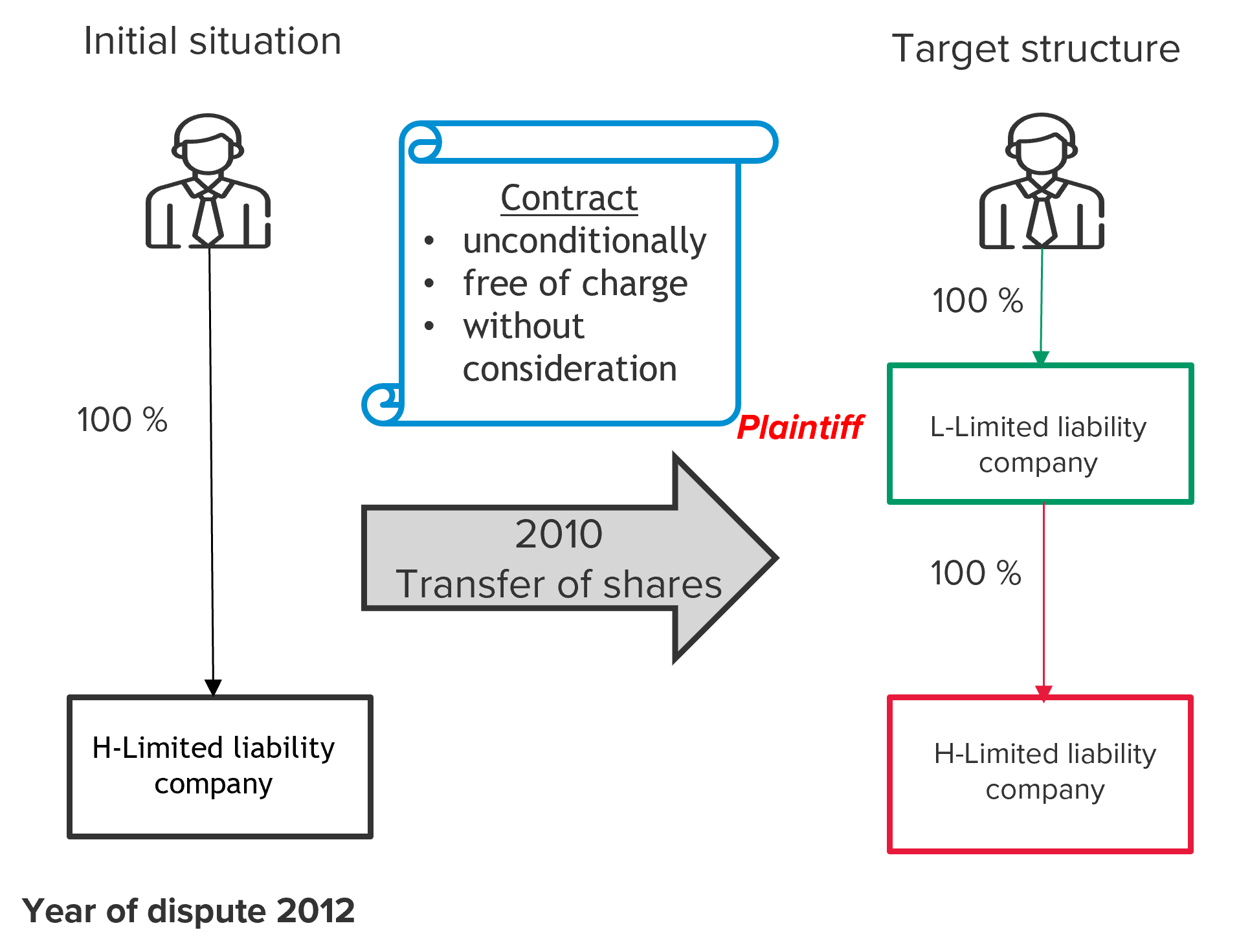

L was the sole shareholder and managing director of H-Limited liability company, which had significant hidden reserves. In 2010, L founded L-Limited liability company as its sole shareholder. By means of a transfer and assignment contract, L transferred his shares in H-Limited liability company, which were held as private assets, to L-Limited liability company on January 1, 2011 free of charge, without conditions and explicitly without consideration, but did not pay any capital gains tax in 2011. L-Limited liability company recorded the transferred shares as at December 31, 2011 at the value of the share capital of H-Limited liability company against capital reserves. However, after the 2011 income tax and corporation tax assessments became final, the tax office increased the income of L-Limited liability company for the disputed year 2012 in accordance with section 8 (3) sentence 4 KStG, as L had secretly transferred his shares in H-Limited liability company, which were held as private assets, to L-Limited liability company, this contribution was to be recognised at its partial value in accordance with section 6 (1) no. 5 of the German Income Tax Act (EStG) and it had reduced L's income due to the failure to tax the capital gain. According to the principle of formal balance sheet consistency, this would lead to an increase in income for L-Limited liability company (only) in the disputed year, as the hidden contribution should have been recognised in the income statement in 2011, but the corporation tax assessment for 2011 was already final.

The BFH disagreed. The excemption provision in section 8 (3) sentence 4 KStG, according to which the hidden contribution must be recognised as increasing income, contrary to the rule in section 8 (3) sentence 3 KStG, does not apply in the case in dispute.

The scope of application of sentence 4 is not limited to cases involving corporations as (investing) shareholders and is also applicable to natural persons. Similarly, the exemption provision does not only cover hidden contributions originating from business assets, but also expressly covers assets from private assets that would generate income upon sale.

However, the failure to tax a (fictitious) capital gain from a share transfer does not lead to a reduction in the income of the hidden shareholder. For this to happen, the hidden contribution must have led to a reduction in the shareholder's income as a basis for taxation, such as through deduction as income-related expenses or business expenses for the shareholder. The non-recognition of a (fictitious) increase in income does not constitute a reduction in income within the meaning of section 8 (3) sentence 4 KStG, but rather a so-called aliud, which is not regulated there. The purpose of the provision, which is to prevent taxation loopholes and ensure that no income adjustment is made if the hidden contribution has ‘reduced’ the shareholder's income, does not require an interpretation that goes beyond the wording of the provision. In particular, there is no risk of taxation loopholes in the case of fictitious capital gains that have been inadvertently omitted, as taxation can be made up for later in the event of a genuine sale.

Notice:

The BFH's clarification that the exemption provision in section 8 (3) sentence 4 KStG only applies in the case of an actual, legally binding reduction in the shareholder's income due to the hidden contribution, in accordance with a literal interpretation of the provision, is to be welcomed by taxpayers. Subsequent correction options for the tax authorities are therefore limited, subject to the option of revoking or amending tax assessments due to new facts or evidence (Section 173 (1) No. 1 to the German Tax Code (AO)).

It remains to be seen whether this ruling represents a trend towards extending the scope of certain legal provisions without clear wording to natural persons. For example, the decision in the appeal proceedings I R 11/24, in which the BFH has to clarify, among other things, whether the deduction prohibition in Section 8b (3) sentence 4 ff. KStG for profit reductions from a loan receivable in connection with participation in other corporations and associations of persons also covers a close relationship with a natural person under certain conditions.