Updates

Date:

If a company’s assets include domestic real estate, the transfer of its shares is subject to real estate transfer tax pursuant to Section 1 (3) No. 1 of the German Real Estate Transfer Tax Act (Grunderwerbsteuergesetz; GrEStG) if this would result in at least 90% (until June 30, 2021; 95%) of the company’s shares being held by the acquirer. In its decision of October 22, 2025 (case no. II R 24/22), the German Federal Fiscal Court (Bundesfinanzhof; BFH) had to assess a case in which a minor acquisition of own shares by a real estate-owning limited liability company (GmbH) triggered a real estate transfer tax liability amounting to millions for its shareholder.

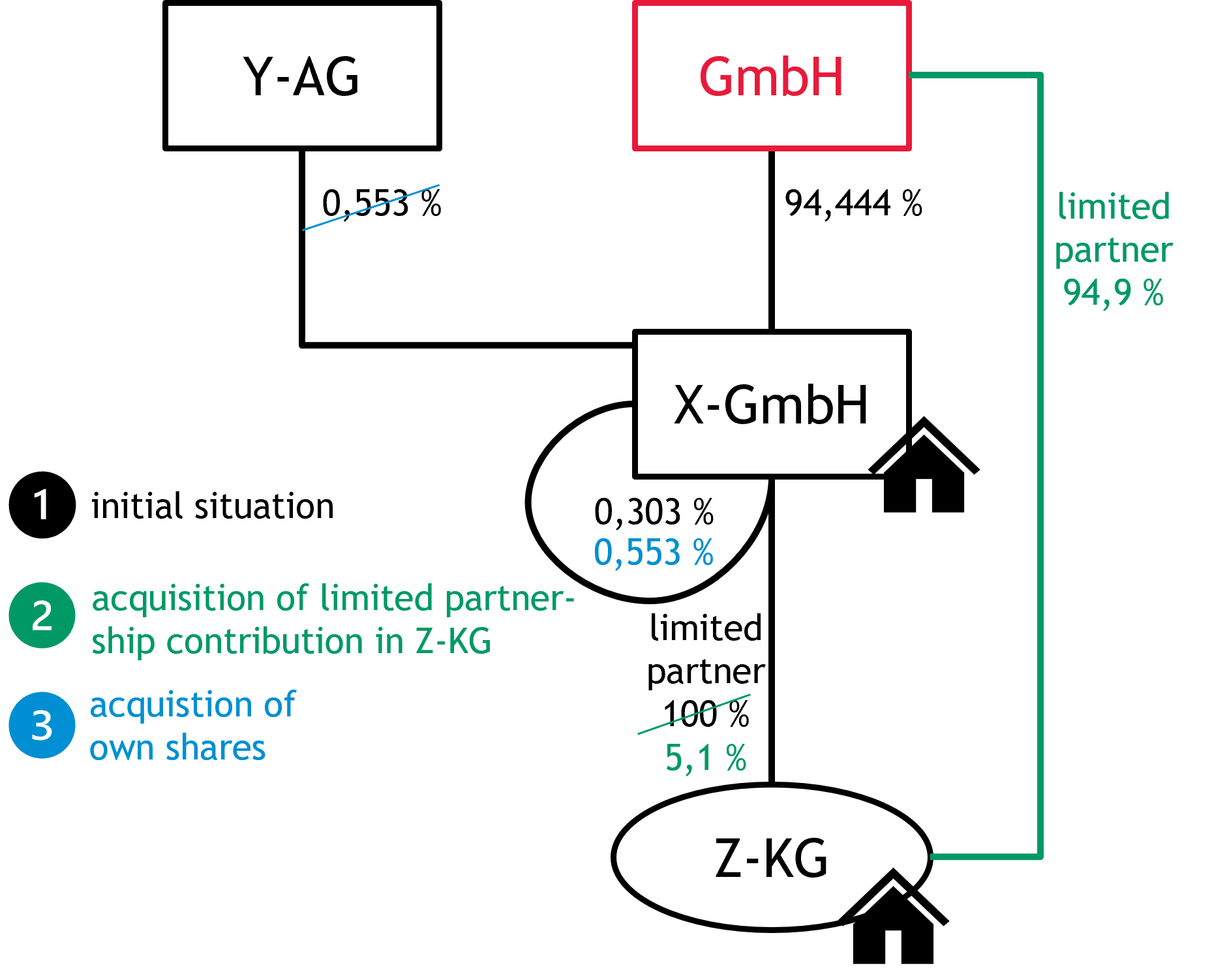

In the case in dispute, the plaintiff GmbH held 94.444% of the shares in X-GmbH, which owned real estate. In addition, Y-AG, among others, held a 0.553% stake in X-GmbH. X-GmbH also held 0.303% of its own shares and was the sole limited partner in Z-KG, which owned real estate.

In 2009, the GmbH acquired 94.9% of the shares in Z-KG; X-GmbH therefore still held a 5.1% stake. In 2010, X-GmbH acquired the shares held in it from Y-AG, so that its own shares now amounted to 0.856%. The notary sent a certified and simple copy of the deed to the tax office regarding the latter share acquisition, requesting that the simple copy be forwarded to the real estate transfer tax office, which did not happen. In 2016, the GmbH informed the tax office that the acquisition of the AG shares by X-GmbH may have resulted in a share consolidation. As a result, the tax office assessed real estate transfer tax of around EUR 6.2 million in November 2017.

Both the first-instance tax court and the BFH agreed with the tax office’s opinion. According to this, due to the acquisition of its own shares by X-GmbH, the shares in this company and in Z-KG held by the GmbH were directly and indirectly combined for the purposes of real estate transfer tax within the meaning of Section 1 (3) No. 1 and No. 2 GrEStG, i.e., it held at least 95% of the shares. When assessing whether the 95% threshold for a direct or indirect consolidation of shares has been reached, own shares held by a corporation as an intermediate company or real estate company are not taken into account. This is because such a company cannot, by definition, be a person other than itself. The acquirer who acquires at least 95% of the shares in the corporation that are not held by the corporation itself controls the corporation's assets in the same way as if the corporation itself did not hold any shares.

In the case in dispute, X-GmbH held a 0.856% stake in its own share capital after acquiring its own shares. Since the shares held by X-GmbH in itself were not to be taken into account in calculating the 95% threshold, the GmbH’s stake in X-GmbH increased to 95.26%. It was irrelevant that the GmbH was not itself the purchaser of the shares and that, under the agreement with X-GmbH, it was entitled to the transfer.

With regard to the properties belonging to Z-KG, there was a partly direct and partly indirect consolidation of shares. Prior to the acquisition of its own shares by X-GmbH, the GmbH held a 94.9% direct stake in Z-KG as a limited partner. As its stake in X-GmbH increased to 95.26%, it was also attributable to it the limited partnership share of X-GmbH amounting to 5.1%, so that it held at least a 95% stake in Z-KG and thus fulfilled the requirements of Section 1 (3) No. 2 GrEStG, since the consolidation had not been preceded by a transaction under the law of obligations within the meaning of

Section 1 (3) No. 1 GrEStG.

At the time the first real estate transfer tax assessment was issued in November 2017, the statute of limitations had not yet expired. This was because, in the absence of effective notification of the acquisition, the assessment period did not begin until the end of the third calendar year following the calendar year in which the tax arose, i.e., the end of 2013. The four-year assessment period therefore ended on December 31, 2017.

Effective notification of the present real estate transfer tax transaction of a share consolidation pursuant to Section 1 (3) No. 1 or No. 2 GrEStG requires that either the certifying notary or the taxpayer report the legal transaction within two weeks of certification or after becoming aware of the transaction subject to notification. This notification must include, among other things, the description of the property according to the land register, cadastre, street and house number, as well as the size of the property and, in the case of developed properties, the type of development. If the company’s assets within the meaning of Section 1 (3) No. 1 GrEStG include several properties, these requirements apply to each individual property. The letter from the notary, in which he merely sent the tax office a certified and simple copy of the deed, is therefore not to be regarded as an effective notification.

Notice:

It is significant that, in the case in dispute, none of the shareholders held at least 95% of the shares in X-GmbH, which owned the property. However, after the latter had acquired a small stake itself, the main shareholder held slightly more than 95%, as the shares held by the company itself were not included in the 95% threshold. The dispute shows once again that share transfers within a group of companies with real estate-owning companies must be carefully structured.