In its ruling of March 11, 2021 ("Danske Bank" C-812/19), the ECJ extended its case law on the taxation of cross-border intra-group supplies between a principal establishment and its branch in the context of the ruling in the "Skandia" case (ruling of Sept. 17, 2014, C-7/13). Affected by this case law are entrepreneurs in Germany and abroad who maintain branches in Germany or another EU member state and mutually exchange services, whereby either the principal establishment or the branch is part of a VAT group in the respective country.

Both the VAT group as interpreted by the EU and the VAT fiscal unity as interpreted by Germany represent group taxation models. Under certain conditions, such models facilitate the service relationships between the individual group members that are to be assessed for VAT purposes; corresponding services are principally non-taxable internal turnover. However, cross-border service relationships must regularly be assessed in accordance with the general rules under EU law. In its ruling of March 11, 2021 (Case No. C-812/19), the ECJ had to answer questions submitted in this regard.

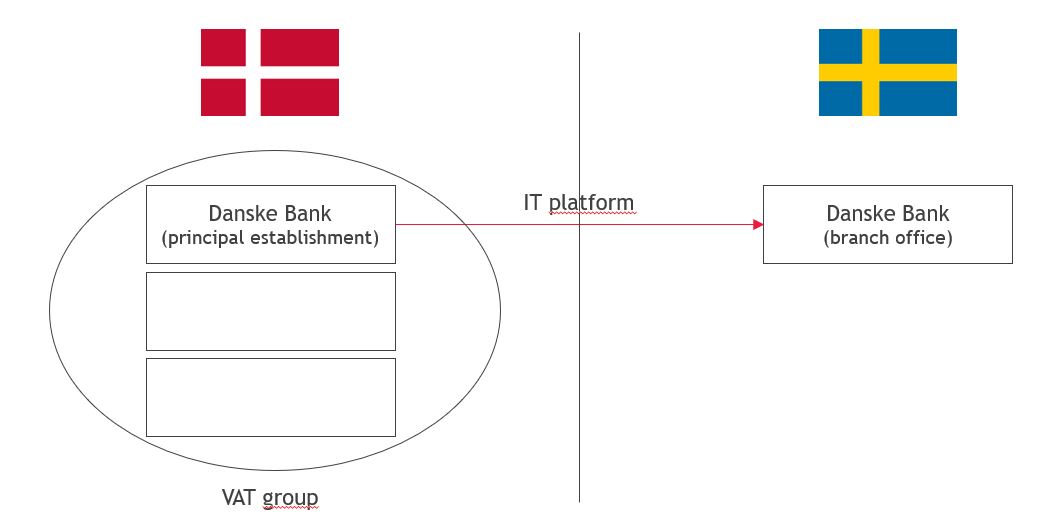

In the matter in dispute, Danske Bank, with its principal establishment in Denmark, was part of a Danish VAT group. The branch held in Sweden was not part of a VAT group. The costs incurred in connection with the provision of an IT platform were charged by the principal establishment to the Swedish branch as non-taxable internal turnover.

The Swedish tax authorities deemed the parties involved to be two separate entrepreneurs, as Danske Bank had separated itself from its Swedish branch by joining the Danish VAT group; the services it provided were to be assessed as taxable transactions, which were taxable in Sweden as reverse charge transactions by the branch. Due to its tax-exempt output transactions, the branch office was not entitled to a VAT deduction in Sweden. The action brought against the ruling with an embedded ECJ referral procedure was ultimately unsuccessful.

Note:

Although the dispute concerns Danish and Swedish VAT law, considering the background of the intended harmonization of VAT law in all EU member states, the decision has enormous significance both for German entrepreneurs who maintain permanent establishments abroad outside their domestic tax group and for domestic permanent establishments with a principal establishment in a third country or another EU member state.

In its argumentation, the ECJ states that a supply between a principal establishment located in a Member State - in this case Denmark - and a branch located in another Member State - in this case Sweden - is in principle not a taxable internal turnover. However, if there is a legal relationship between the provider of the service and the recipient, in particular because one of the two parties is part of a VAT group, taxable service relationships exist. This is because the ECJ assumes that, as a result of the association in the VAT group, the services are supplied by the group. In this respect, it is irrelevant whether the group is made up of a parent company or a subsidiary company.

In the case in dispute, it must therefore be assumed that the IT services provided to the Swedish branch office are provided by the Danish VAT group as a whole. In this context, the Swedish branch office cannot be part of the Danish VAT group with regard to the territorial restrictions stipulated under EU law. Ultimately, therefore, the two parties - also pursuant to the ECJ ruling of 17.09.2014 in the Skandia America Corp. (Case C-7/13) - are not to be deemed as a single taxable person.

In the Skandia America Corp. legal case, the ECJ ruled that the service provided by a principal establishment located in a third country to a branch located in the EU constitutes a taxable transaction if the branch belongs to a VAT group. In the opinion of the ECJ, such membership overlaps the connection between the principal/main establishment and the branch office, so that there was no internal turnover but a taxable supply of services. Since the services were provided, the reverse charge procedure was applied, so that the branch office was liable for the VAT. However, it could not claim a VAT deduction due to tax-exempt output sales. As a result, VAT became a real cost factor.

Note:

A draft BMF letter issued in 2018 proposed to limit the principles of the Skandia ruling to third country cases. However, for lack of implementation, the administrative opinion at the time remained that non-taxable intra-company transactions were to be assumed between the principal establishment and the branch - much to the delight of banks and insurance companies in particular, which regularly cannot claim any or only a small VAT deduction, but are set up cross-border with branch offices.

In the wake of the ECJ ruling in the Danske Bank case, a clarifying BMF letter or an amendment to the UStAE is overdue. We will continue to monitor the further development for you.

Banks and insurance companies are particularly affected by this ruling. They should therefore review their VAT position in each country to determine whether a principal or branch office is part of a VAT group and also provides services to a branch located in another country. If necessary, the dissolution of tax group relationships or the division of areas of activity should be considered in order to save the VAT deduction. We will be happy to support you in reviewing and reorganizing the structures affected by this court ruling.